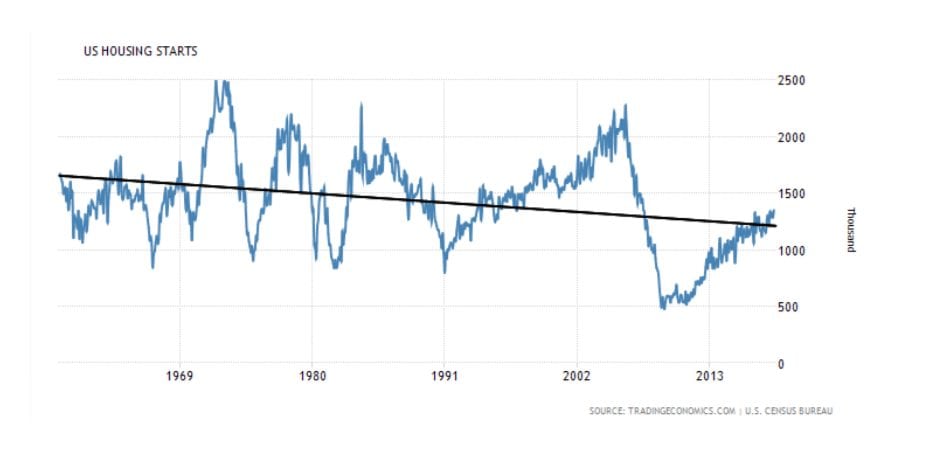

Housing start stats. You’ve got to love them.

One month they’re up, the next month they’re down. What’s an astute investor to make of this?

To begin with, it’s never a good idea to pay too much attention to month-over-month housing trends. That’s because the timeline is simply too short.

Real estate developers can spend years jumping through the hoops that local municipalities, state governments, and the EPA place in their path of development. Only to see their project eventually fall through due to regulatory issues or a change in the real estate market.

When that happens, the housing units in the construction project that were counted as starts suddenly turn into stops. Housing stops aren’t reflected in any official housing market data, only in the GDP several years down the road.

As we’ve written before, statistics should always be taken with a grain of salt. The one statistic that doesn’t lie, the one that none of us can escape, is age.

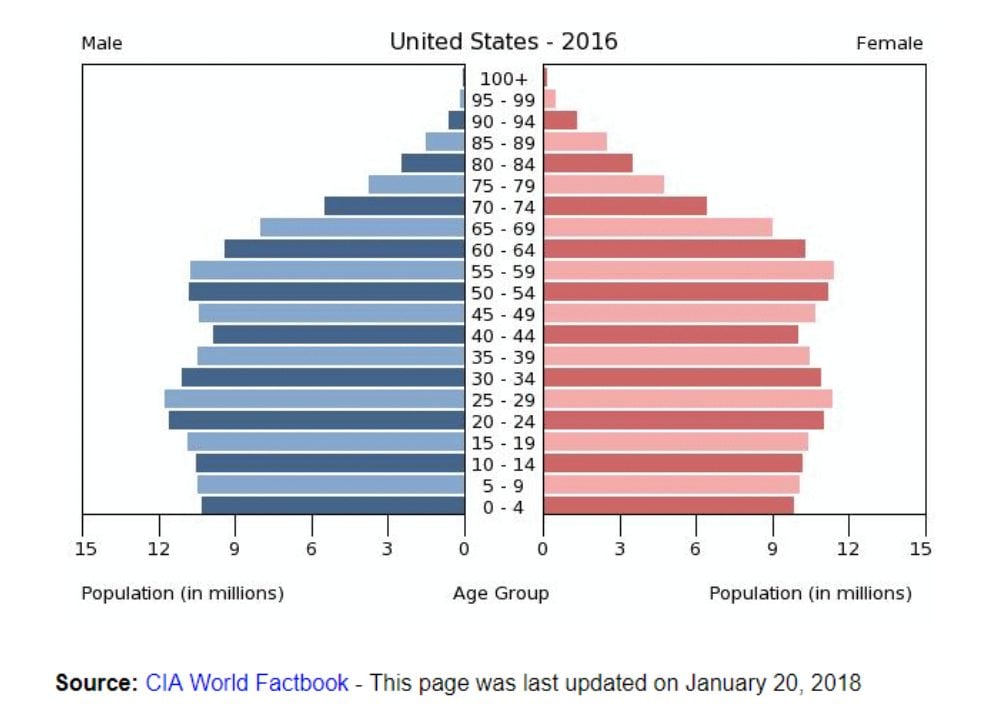

To forecast what’s in store for U.S. housing market starts it’s instructive to look at the population age groups as they move forward over time. We’ll begin with the U.S., then hop over to Japan, whose aging population is about 10 years ahead of the United States.

Currently, nearly 30% of the people in the U.S. are 55 years of age or older. Another 26% are between the ages of 35 and 54.

And while the seniors of today and tomorrow don’t and likely won’t act like the senior citizens of yesteryear, the one thing that all seniors have in common is the need to spend more money on health care as they get older.

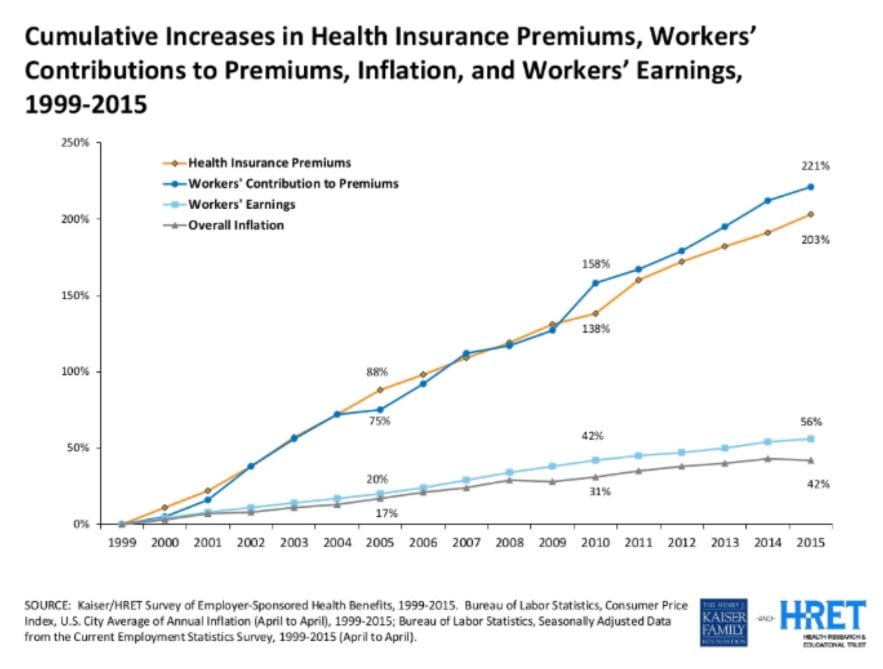

A joint report by the Kaiser Family Foundation and Health Research & Educational Trust illustrates just how much health care costs have outpaced wage growth during the past 15 years.

Over that time-period workers’ earnings have grown by about 56% while inflation has increased by about 42%. That’s an average inflation-adjusted increase in wages of only 1% per year.

By comparison, both health insurance premiums and workers’ contribution to premiums have increased by over 200% during the same 15-year period.

Absent a silver bullet by the government to reign in rising medical costs seniors will be forced to spend an increasing amount of their money on health care and less on things like housing.

Which means that housing starts will continue to decline going forward. Not because of issues such as unaffordable houses, lack of developable land, or government interference. But simply due to lack of demand as the U.S. population is getting older.

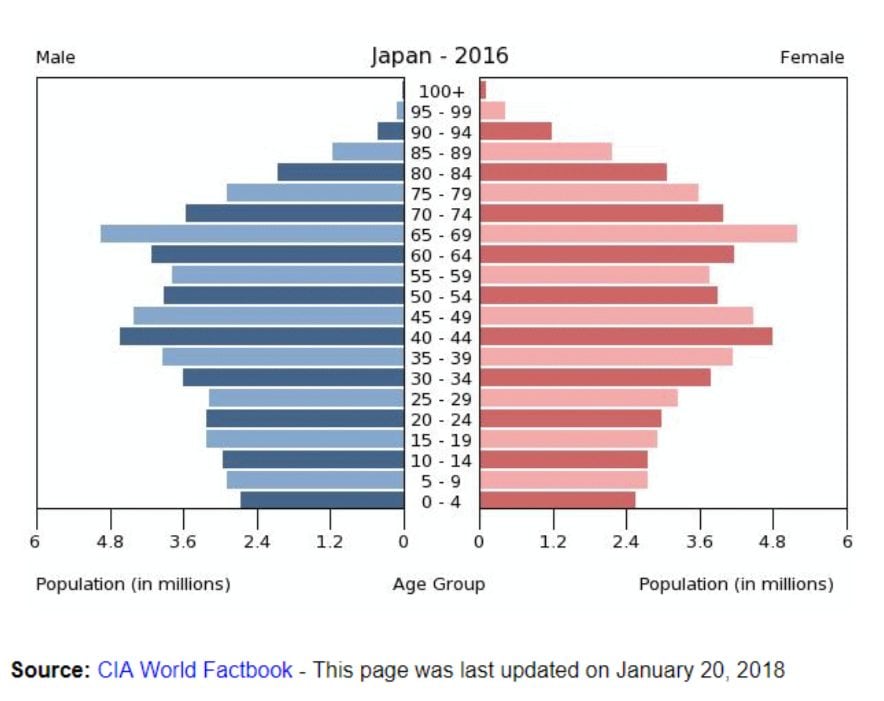

Now let’s cross the Pacific Ocean and head over to Japan, a market whose aging population is 10 years or so ahead of the U.S. In Japan over 40% of the people are 55 years are older. That’s over one-third more than in the U.S.

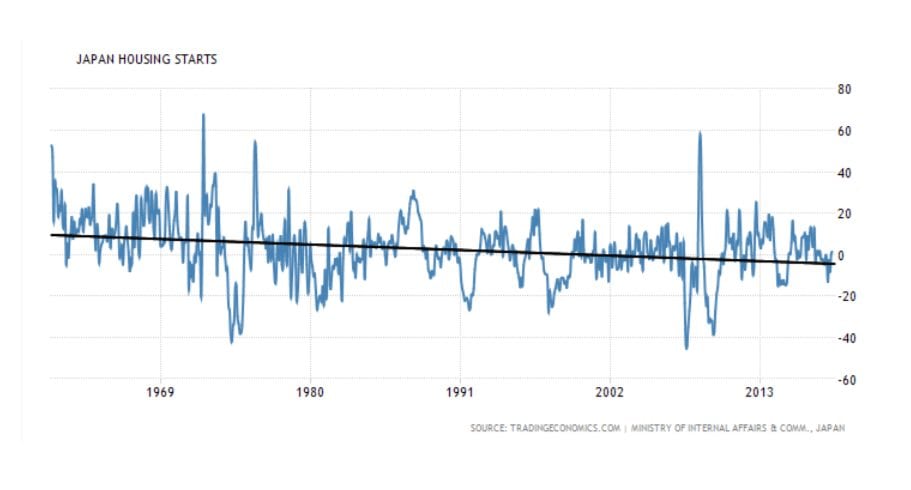

The effect that an older population like this has had on housing starts is remarkable.

While month-to-month housing start stats are as erratic in Japan as they are in the U.S., Japan’s longer-term housing starts have been essentially flat. As people in the United States age, it’s likely that this country’s housing starts will continue to decline as well.

Although that doesn’t bode well for home builders, this decline does present a window of opportunity for investment in long-term care facilities and senior living.

References:

[button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://tradingeconomics.com/united-states/housing-starts” text=”View Trading Economics Article” color_override=””] [button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://www.kff.org/other/state-indicator/distribution-by-age/” text=”View Kaiser Family Foundation Article” color_override=””] [button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://www.indexmundi.com/united_states/age_structure.html” text=”View Index Mundi Article” color_override=””] [button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://www.healthpopuli.com/2015/09/23/health-consumers-cost-increases-far-outpace-wage-growth/” text=”View Health Populi Article” color_override=””] [button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://www.indexmundi.com/japan/age_structure.html” text=”View Index Mundi Article 2″ color_override=””] [button open_new_tab=”true” color=”accent-color” hover_text_color_override=”#fff” size=”medium” url=”https://tradingeconomics.com/japan/housing-starts” text=”Read Trading Economics Article 2 ” color_override=””]

Join Our Newsletter!